A Strategy for Predictable High Monthly Income in Retirement

Structured Income Flash Notes

Looking for Predictable High Monthly Income without the unnecessary risk?

Structured Income Flash Notes are designed to provide guaranteed high monthly income linked to major market indexes — with built-in protection barrier with just a 12-month commitment.

If you're transitioning into retirement and want a high income that’s dependable, consistent, and with moderate to low risk, this may be worth a conversation.

Retirement changes how you think about money.

And for many investors, that unpredictability becomes harder to accept over time.

Why traditional strategies can fall short

- Real returns may be reduced by taxes and inflation

- A 60/40 portfolio still relies heavily on market performance

- Some annuities can restrict access to your capital

- Dividend income can fluctuate with market conditions

Who This May Be Right For

A Structured Income Flash Note may be worth considering if:

Predictablity

You are pivoting toward retirement and want a predictable high monthly income.

Alternative to Bonds

You want higher income potential than traditional bonds.

Defined Terms

You prefer defined one-year terms rather than open-ended market exposure.

Introducing Structured Income Flash Notes

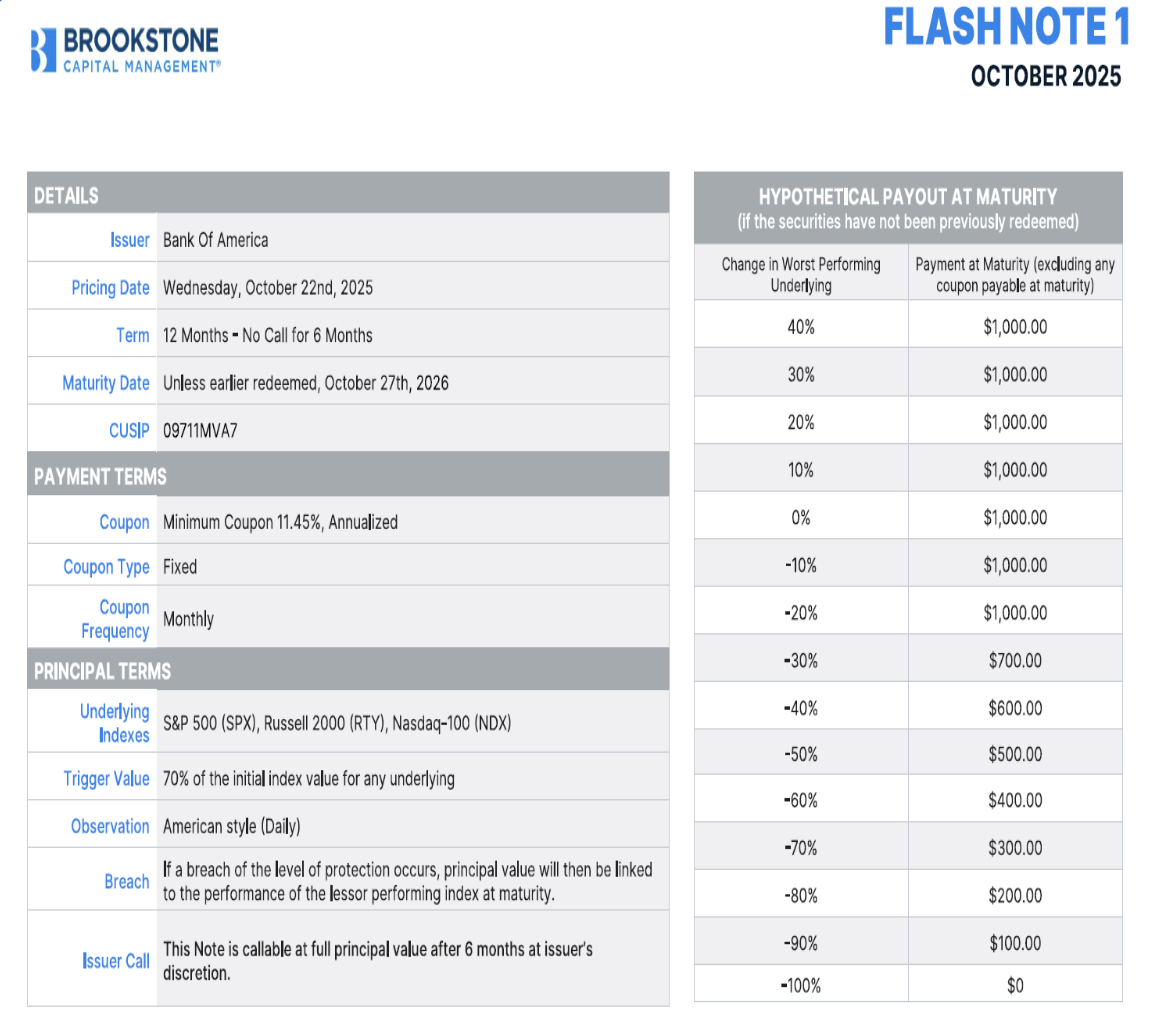

Structured Income Flash Notes are short-term debt securities linked to major stock market indexes, designed to provide defined monthly income.

- Issued by major financial institutions

- 12-month term

- High-yield coupon (often in the 10% - 12% range depending on offering)

- Monthly interest payments

- Linked to the S&P 500, Nasdaq-100, and Russell 2000

- 30% barrier before principal is impacted at maturity

These are not FDIC-insured and do involve risk, including potential loss of principal. But for investors with a moderately conservative risk profile (often categorized as a 2 on a 1–5 scale), they can provide a structured alternative to traditional income strategies

Issued by major financial institutions

12-month term

High-yield coupon (often in the 10% - 12% range depending on offering)

Monthly interest payments

Linked to the S&P 500, Nasdaq-100, and Russell 2000

30% barrier before principal is impacted at maturity

Why Haven’t You Heard of These Before?

Structured income flash notes aren’t products you can log in and buy like a mutual fund. They are negotiated directly with major banks in the capital markets, one issuance at a time.

Peter Garcia of My Legacy Group partners with Brookstone Capital Management to make these offerings available to private clients with a moderate conservative risk profile.

Are Structure Income Flash Notes right for you?

Here is a simple plan to move forward:

1. Confirm Suitability

We review your goals, timeline, and risk tolerance to determine whether this fits your broader retirement plan.

2. Structure the Account

Open an individual, joint, or IRA account and determine allocation between individual Flash Notes, the Booster Income Fund, or a blend.

3. Begin Receiving Monthly Income

Once allocated, defined interest payments begin monthly, based on the terms of each offering

Important Considerations

Structured Income Flash Notes:

- Are not FDIC insured

- Require a 12-month commitment

- Carry risk, including potential loss of principal

- Are tied to market performance and subject to issuer credit risk

They are designed for investors who understand the trade-offs and want income structured around defined terms rather than open-ended market exposure.